The United States subprime mortgage crisis is a national banking emergency, occurring between 2007-2010, which contributed to the US recession in December 2007-June 2009. This was sparked by a large drop in house prices after the collapse of the housing bubble, which leading to mortgage delinquency and foreclosure and devaluation of housing-related securities. The decline in housing investment precedes the recession and is followed by a reduction in household spending and then business investment. The reduction in spending is more significant in areas with a combination of high household debt and larger housing price reductions.

The housing bubble that preceded the crisis was financed with mortgage backed securities (MBS) and collateralized debt obligations (CDO), which initially offered higher interest rates (ie better returns) of government securities, along with an attractive risk rating from rating agencies. While the elements of the first crisis became more visible during 2007, several major financial institutions collapsed in September 2008, with significant disruptions in the flow of credit to businesses and consumers and the onset of a severe global recession.

There are many causes of the crisis, with commentators assigning various levels of error to financial institutions, regulators, credit agencies, government housing policies, and consumers, among others. The two closest causes are increases in subprime lending and increased housing speculation. The percentage of poor-quality subprime mortgages that originated during a given year rose from a range of 8% or lower that historically to about 20% from 2004 to 2006, with a much higher ratio in some parts of the US. A high percentage of this subprime mortgage, above 90% in 2006 for example, is a mortgage with an adjustment rate. Housing speculation has also increased, with the share of mortgage originations to investors (ie those with homes other than primary residence) increased significantly from about 20% in 2000 to about 35% in 2006-2007. Investors, even those with excellent credit ratings, are much more likely to fail than non-investors when prices go down. This change is part of a broader trend of lower loan standards and high-risk mortgage products, which contributes to US households becoming increasingly indebted. The ratio of household debt to disposable personal income increased from 77% in 1990 to 127% by the end of 2007.

When US home prices declined sharply after peaking in mid-2006, it became more difficult for borrowers to refinance their loans. Because adjusted mortgage rates start reset with higher interest rates (leading to higher monthly payments), mortgage delinquency increases. Securities backed by mortgages, including subprime mortgages, which are widely held by global financial firms, lose most of their value. Global investors also drastically reduced purchases of mortgage-backed debt and other securities as part of the decline in the capacity and willingness of the private financial system to support lending. Concerns about the health of credit and US financial markets are causing tightening of credit around the world and slowing economic growth in the US and Europe.

The crisis has heavy long-term consequences for the US and European economies. The US entered a deep recession, with nearly 9 million jobs lost during 2008 and 2009, about 6% of the workforce. The number of jobs did not return to pre-crisis peaks in December 2007 through May 2014. US household net worth declined nearly $ 13 trillion (20%) from the 2007 Q2 pre-crisis peak, recovering in Q4 2012. US housing prices fell nearly 30% average and US stock markets fell by about 50% in early 2009, with stocks regaining December 2007 levels during September 2012. One estimate of output losses and revenues from the crisis came to "at least 40% of 2007 gross domestic product". Europe also continues to struggle with its own economic crisis, with high unemployment and severe banking damage estimated at EUR940 billion between 2008 and 2012. In January 2018, US bailouts have fully recovered by the government, when interest on loans was taken into consideration. A total of $ 626B was invested, loaned, or granted for various bailout actions, while $ 390B had been returned to the Treasury. The Treasury has received another $ 323 billion in interest on a bailout loan, generating a profit of $ 87B.

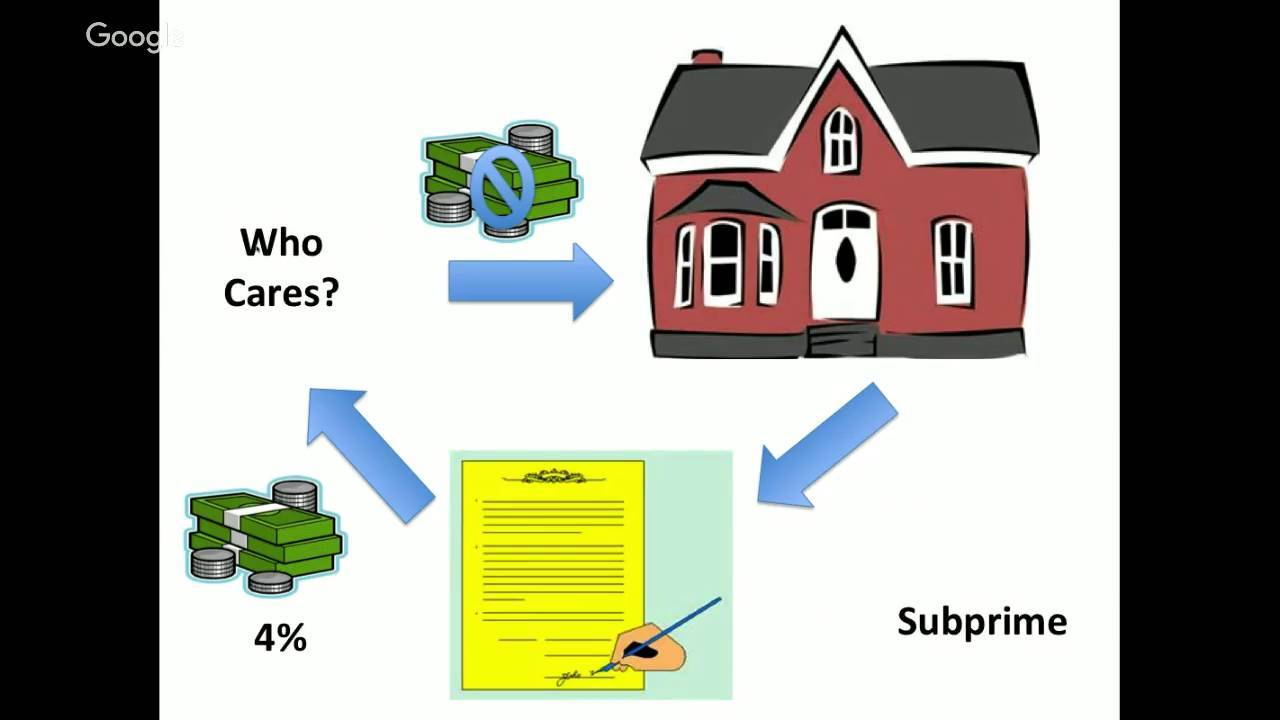

Video Subprime mortgage crisis

Background and timeline of events

The immediate cause or trigger of the crisis is the bursting of the housing bubble of the United States that peaked in about 2005-2006. Increased loan incentives such as easy initial requirements and long-term housing price hike trends have prompted borrowers to endure risky mortgages in anticipation that they will be able to quickly refinance more easily. However, once interest rates begin to rise and housing prices begin to moderate in 2006-2007 in many parts of the US, borrowers can not refinance. Default activity and foreclosures are increasing dramatically due to preliminary early requirements, falling house prices, and adjusted interest rate mortgage rates (RET) higher resets.

When house prices fall, global investor demand for mortgage-related securities evaporates. This became clear in July 2007, when the investment bank Bear Stearns announced that two hedge funds had exploded. These funds have been invested in securities that derive their value from the mortgage. When the value of these securities falls, investors ask that hedge funds provide additional guarantees. This creates a sales cascade in these securities, which decreases its value even further. Economist Mark Zandi writes that the 2007 event was "arguably the ultimate catalyst" for the disruption of financial markets that followed.

Several other factors set the stage for a rise and fall in housing prices, and related securities held widely by financial firms. In the years leading up to the crisis, the United States received large sums of foreign money from the rapidly developing countries of Asia and oil-producing countries/exporters. The flow of these funds combined with low US interest rates from 2002 to 2004 contributed to easy credit conditions, which triggered housing and credit bubbles. Loans of various types (eg, mortgages, credit cards, and auto) are easy to obtain and consumers assume an unprecedented debt burden.

As part of housing and credit booms, the number of financial agreements called mortgage-backed securities (MBS), which derive their value from mortgage payments and home prices, is greatly increased. This kind of financial innovation allows institutions and investors around the world to invest in the US housing market. As housing prices decline, the major global financial institutions that have borrowed and invested heavily in MBS reported significant losses. Default and losses on other types of loans also increased significantly as the crisis expanded from the housing market to other parts of the economy. Total losses are estimated in trillions of US dollars globally.

While housing and credit bubbles are growing, a number of factors cause the financial system to become increasingly fragile. Policymakers do not recognize the increasingly important role played by financial institutions such as investment banks and hedge funds, also known as the shadow banking system. These entities are not subject to the same rules as storage banks. Furthermore, shadow banks are able to cover their risk-taking levels from investors and regulators through the use of complex off-balance sheet derivatives and securitization. Economist Gary Gorton refers to the aspect of the 2007-2008 crisis as a "run" on the shadow banking system.

The complexity of setting up off-balance sheets and securities owned, as well as the interconnection between larger financial institutions, makes it almost impossible to rearrange them through bankruptcy, which contributes to the needs of government bailouts. Some experts believe that these shadow agencies become as important as commercial banks (deposits) in giving credit to the US economy, but they are not subject to the same rules. These institutions as well as certain regulated banks have also assumed a significant debt burden while providing the loans described above and do not have sufficient financial bearings to absorb large loan defaults or MBS losses.

Losses experienced by financial institutions in securities related to their mortgages have an impact on their ability to lend, slowing economic activity. The interbank loan was dry initially and then the loan to non-financial companies was affected. Concerns about the stability of major financial institutions pushed central banks to take action to provide funds to encourage lending and to restore confidence in the commercial paper market, which is an integral part of business operations funding. The Government also provides guarantees to major financial institutions, assuming significant additional financial commitments.

The risks to the wider economy created by the housing market downturn and subsequent financial market crises are a major factor in some decisions by central banks around the world to cut interest rates and the government to implement an economic stimulus package. The effect on global stock markets because of the crisis was dramatic. Between 1 January and 11 October 2008, shareholders in US companies suffered losses of about $ 8 trillion, as their holdings declined from $ 20 trillion to $ 12 trillion. Losses in other countries averaged about 40%.

Losses in the stock market and declining housing values ​​put further downward pressure on consumer spending, the main economic engine. The leaders of the larger developed and developing countries met in November 2008 and March 2009 to formulate strategies to overcome the crisis. Various solutions have been proposed by government officials, central bank governors, economists, and business executives. In the US, Dodd-Frank Wall Street Reform and the Consumer Protection Act were signed into law in July 2010 to address several causes of the crisis.

Maps Subprime mortgage crisis

Cause

Overview

The crisis can be attributed to many pervasive factors in both credit markets, factors that have emerged over the years. The proposed causes include the inability of the homeowner to make mortgage payments (mainly due to adjustments of re-adjusted mortgages, borrowers over limit, predatory borrowing, and speculation), overbuilding during boom periods, risky mortgage products, increased mortgage holder, high personal and corporate debt levels, distributed financial products and may hide the risk of credit defaults, poor monetary and housing policies, international trade imbalances, and inaccurate government regulations. Excessive consumer housing debt is in turn caused by mortgage backed securities, credit default swaps, and collateralized debt obligations in the financial industry sub-sector, offering irrational low rates and high levels of irrational agreements for subprime mortgage consumers because they count aggregate risks using the copula gaussian formula that strictly assumes the independence of individual component mortgages, when in fact the creditworthiness of almost every new subprime mortgage is highly correlated with others because of the linkage through the level of consumer spending that drops sharply when property values ​​begin to fall during the initial wave of default mortgages. Debt consumers act in their rational personal interests, because they can not audit the methodology of fixing risky financial industry risks.

Among the important catalysts of the subprime crisis are the inflow of money from the private sector, banks entering the mortgage bond market, government policies aimed at expanding home ownership, speculation by many home buyers, and mortgage borrowing lending practices, particularly tailored rate mortgages, -28, mortgage lenders sold directly or indirectly through mortgage brokers. On Wall Street and in the financial industry, moral hazard is at the heart of many causes.

In the "Declaration of the Summit on Financial Markets and the World Economy," dated 15 November 2008, leaders of Group 20 mentioned the following causes:

During periods of strong global growth, rising capital flows, and prolonged stability early in the decade, market participants sought higher yields without adequate appreciation of risk and failed due diligence. At the same time, underwriting standards are weak, unhealthy risk management practices, increasingly complex and opaque financial products, and consequently excessive leverage is combined to create vulnerabilities in the system. Policymakers, regulators and regulators, in some developed countries, do not adequately value and cope with rising risks in financial markets, following financial innovations, or considering the systemic consequences of domestic regulatory measures.

Federal Reserve Chairman Ben Bernanke testified in September 2010 about the causes of the crisis. He writes that there are shocks or triggers (ie certain events that touch the crisis) and vulnerability (ie structural weaknesses in the financial system, regulation and supervision) that reinforce shocks. Examples of triggers include: a loss on subprime mortgage securities that began in 2007 and ran on a shadow banking system that began in mid 2007, adversely affecting the functioning of the money market. Examples of vulnerabilities in the private sector include: the dependence of financial institutions on unstable short-term funding sources such as repurchase agreements or Repo; deficiencies in corporate risk management; excessive use of leverage (borrowing to invest); and the use of inappropriate derivatives as a tool to take excessive risks. Examples of vulnerabilities in the public sector include: legal gaps and conflicts among regulators; ineffective use of regulatory authorities; and ineffective crisis management skills. Bernanke also discussed the "Too big to fail" institution, monetary policy, and trade deficit.

During May 2010, Warren Buffett and Paul Volcker separately described the dubious assumptions or judgments underlying the US financial and economic system that contributed to the crisis. These assumptions include: 1) housing prices will not fall dramatically; 2) A free and open financial market supported by sophisticated financial engineering will most effectively support market efficiency and stability, directing funds to the most profitable and productive use; 3) The concepts embedded in mathematics and physics can be directly adapted to the market, in the form of various financial models used to evaluate credit risk; 4) Economic imbalances, such as large trade deficits and low savings rates that indicate excessive consumption, are sustainable; and 5) Stronger arrangements of shadow banking systems and derivative markets are not required. Economists surveyed by the University of Chicago during 2017 assessed the factors that caused the crisis in order of importance: 1) Arrangement and supervision of the defective financial sector; 2) Underestimating the risks in financial engineering (eg, CDO); 3) Mortgage fraud and bad incentives; 4) Short-term and appropriate funding decisions in those markets (e.g., Repo); and 5) Failure of credit rating agencies.

The US Financial Crisis Investigation Commission reported its findings in January 2011. It concludes that "the crisis can be avoided and caused by: Widespread failure in financial regulation, including the failure of the Federal Reserve to stem the tide of toxic mortgages: dramatic damage to corporate governance including too many financial companies who are acting recklessly and taking too much risk: The explosive mix of excessive loans and risks by households and Wall Street puts the financial system in a collision with the crisis: The major policymakers are not ready for the crisis, lacking a full understanding of the financial system they observe and systemic violations in accountability and ethics at all levels. "

Narration

There are some "narratives" that try to put the causes of crisis into context, with overlapping elements. Five such narratives include:

- There is an equivalent of a bank run on a shadow banking system, which includes investment banks and other non-depository financial entities. This system has grown to rival storage systems on a scale but is not subject to the same security protection.

- The economy is driven by a housing bubble. When exploded, private residential investment (ie, housing construction) fell by almost 4% of GDP and the consumption made possible by the wealth of housing generated by bubbles also slowed. This creates a gap in annual demand (GDP) of nearly $ 1 trillion. The government does not want to cover the shortage of the private sector.

- The amount of household debt records collected in the decades before the crisis resulted in a balance sheet recession (similar to debt deflation) as home prices began falling in 2006. Consumers began paying off debts, which reduced their consumption, slowed the economy for a period of time long while the debt rate is reduced.

- Housing speculation using high mortgage debt levels is driving many investors with prime quality mortgages (ie, investors amid the distribution of credit scores) to defaults and entering foreclosures of investment properties when house prices fall; blamed on homeowners "subprime" (ie, those who are at the bottom of the credit score distribution) is overstated.

- Government policies that encourage homeownership even for those who can not afford it, contribute to loose loan standards, unsustainable housing price increases and debt.

The underlying narrative of # 1-3 is the hypothesis that increased income inequality and wage stagnation encourage families to increase their household debt to maintain the standard of living they desire, encouraging bubbles. Furthermore, the lion's share of upward-flowing income increases the political power of business interests, which uses that power to deregulate or limit the regulation of the shadow banking system.

Housing market

Boom and bust

According to Robert J. Shiller and other economists, the rise in housing prices outside the general inflation rate is not sustainable in the long run. From the end of World War II to the beginning of the housing bubble in 1997, housing prices in the US remained relatively stable. The bubble is characterized by higher household debt levels and lower savings rates, slightly higher homeownership rates, and of course higher house prices. Fueled by low interest rates and a large flow of foreign funds that creates easy credit conditions.

Between 1997 and 2006 (housing bubble peak), typical American home prices increased by 124%. From 1980 to 2001, the ratio of average house price to average household income (size of ability to buy a home) fluctuated from 2.9 to 3.1. In 2004 it rose to 4.0, and in 2006 reached 4.6. The housing bubble is more prominent in coastal areas where the ability to build new housing is limited by geographical or land use restrictions. These housing bubbles generate enough homeowners who refinance their homes with lower interest rates, or finance consumer spending by taking a second mortgage guaranteed by price appreciation. US household debt as a percentage of annual disposable personal income was 127% at the end of 2007, compared to 77% in 1990.

While house prices are rising, consumers save less and both borrow and spend more. Household debt grew from $ 705 billion at the end of 1974, 60% of disposable personal income, to $ 7.4 trillion by the end of 2000, and eventually to $ 14.5 trillion by mid 2008, 134% of personal income disposable. During 2008, ordinary US households had 13 credit cards, with 40% of households having balances, up from 6% in 1970.

The free cash used by consumers from home equity extraction doubled from $ 627 billion in 2001 to $ 1.428 billion in 2005 when a housing bubble was built, totaling nearly $ 5 trillion over the period. US home mortgage debt relative to GDP increased from an average of 46% during the 1990s to 73% during 2008, reaching $ 10.5 trillion. From 2001 to 2007, US mortgage debt doubled, and the amount of mortgage debt per household increased by more than 63%, from $ 91,500 to $ 149,500, with essentially stagnant wages. Economist Tyler Cowen explains that the economy relies heavily on the extraction of home equity: "In the period 1993-1997, homeowners extracted some equity from their homes equivalent to 2.3% to 3.8% of GDP.In 2005, this number has increased to 11.5% of GDP. "

The explosion in price and house prices caused a building boom and eventually became a surplus of unsold homes, causing US housing prices to peak and beginning to decline in mid-2006. Easy credit, and confidence that house prices will continue to rise, has prompted many borrowers subprime to get a mortgage with adjustable interest rates. This mortgage lures the borrower with below market interest rates for some predetermined period, followed by market rates for the remaining term of the mortgage.

US home ownership rates increased from 64% in 1994 (approximately since 1980) to an all-time high of 69.2% in 2004. Subprime lending is a major contributor to an increase in the level of homeownership and in overall demand for housing, which pushed prices higher.

Borrowers who will not be able to make higher payments after the initial grace period expire, plan to refinance their mortgage after a year or two year award. As a result of depreciating housing prices, the borrower's ability to refinance becomes more difficult. Borrowers who find themselves unable to escape a higher monthly payment by refinancing start default.

As more and more borrowers stop making mortgage payments, foreclosures and home supplies for sale increase. This puts downward pressure on housing prices, which further lowers the homeowner's equity. The decline in mortgage payments also reduced the value of mortgage-backed securities, which undermined the net worth and financial health of banks. This vicious circle is at the heart of the crisis.

As of September 2008, the average US house price declined by more than 20% from its peak in mid 2006. This large and unexpected drop in house prices meant that many borrowers had zero or negative equity in their homes, which meant their home was worth lower than their mortgage. In March 2008, an estimated 8.8 million borrowers - 10.8% of all homeowners - had negative equity in their homes, a number believed to have risen to 12 million by November 2008. As of September 2010, 23% of all US homes were worth less than a mortgage loan.

Borrowers in this situation have an incentive to default on their mortgage because the mortgage is usually a non-debt guarantee that is secured against the property. Economist Stan Leibowitz argues in the Wall Street Journal that even though only 12% of homes had negative equity, they made up 47% of foreclosures during the second half of 2008. He concluded that home equity levels are a key factor in foreclosures, rather than types of loans, creditworthiness borrowers , or ability to pay.

Increased foreclosure rates increase the supply of homes offered for sale. The number of new homes sold in 2007 was 26.4% lower than in the previous year. In January 2008, the inventory of new unsold homes was 9.8 times the December 2007 sales volume, the highest value of this ratio since 1981. In addition, nearly four million homes were sold, with approximately 2.2 million vacant homes.

The closure of the unsold house reduced the price of the house. When prices are falling, more homeowners are at risk of default or foreclosure. House prices are expected to continue to decline until this unsold supply of homes (eg excess supply) declines to normal levels. A report in January 2011 stated that the value of US homes fell 26 percent from its peak in June 2006 to November 2010, more than the 25.9 percent decline between 1928 and 1933 when the Great Depression took place.

From September 2008 to September 2012, there are about 4 million foreclosures completed in the US. In September 2012, around 1.4 million homes, or 3.3% of all homes with mortgages, were in foreclosure stages compared to 1.5 million, or 3.5%, in September 2011. During September 2012, 57,000 homes finished confiscated; this was down from 83,000 before September but well above the 2000-2006 average of 21,000 completed foreclosures per month.

Owners home speculation

Speculative loans in residential real estate have been cited as a contributing factor to the subprime mortgage crisis. During 2006, 22% of purchased homes (1.65 million units) were for investment purposes, with an additional 14% (1.07 million units) purchased as holiday homes. During 2005, these figures were 28% and 12%, respectively. In other words, a record level of nearly 40% of purchased homes is not intended to be a primary residence. David Lereah, chief economist at the National Association of Realtors at the time, stated that the decline in investment purchases in 2006 is expected: "Speculators left the market in 2006, causing investment sales to fall much faster than the primary market."

Housing prices almost doubled between 2000 and 2006, a trend that is much different from the historical appreciation of the inflation rate. Although homes are not traditionally treated as investments that are influenced by speculation, this behavior changes during the housing boom. The media reported condos that were bought while under construction, then "reversed" (sold) for profit without the seller ever living in them. Some mortgage companies identified the risks inherent in this activity in early 2005, after identifying investors with the assumption of highly leveraged positions in some properties.

One NBER 2017 study states that real estate investors (ie, those with 2 houses) are more blamed for the crisis than the subprime borrowers: "The increase in mortgage defaults during a crisis is concentrated amid the distribution of credit scores, and largely due to real estate investors" and that "credit growth between 2001 and 2007 is concentrated in key segments, and debt for high-risk borrowers [subprime] is almost constant for all debt categories during this period." The authors argue that this investor-driven narrative is more accurate than blaming the crisis on borrowers low income subprime. The 2011 Fed study has similar findings: "In countries that experienced the biggest housing booms and busts, at the top of the market almost half of the origination mortgage purchases were attributed to investors, partly because it seems wrong to report their intention to occupy the property, investors are taking more leverage , contributing to a higher failure rate. "The Fed study reported that mortgage origins for investors increased from 25% in 2000 to 45% in 2006, to Arizona, California, Florida, and Nevada as a whole, where housing prices are rising during bubbles (and decreases in bust) are most prominent. In these countries, investor losses increased from about 15% in 2000 to over 35% in 2007 and 2008.

Nicole Gelinas of the Manhattan Institute illustrates the negative consequences of not adjusting tax and mortgage policies with shifting cultivation from a conservative inflation hedge to a speculative investment. Economist Robert Shiller argues that the speculative bubble is triggered by "infectious optimism, which seems to be immune to the facts, which often occur when prices are rising.Bubbles are primarily social phenomena, until we understand and overcome the psychology that fuel them, forming. "Keynesian economist Hyman Minsky describes how speculative loans contribute to rising debt and ultimately collapse of asset values.

Warren Buffett testified to the Financial Crisis Inquiry Commission: "There was the greatest bubble I've ever seen in my life... The entire American public eventually caught up in the belief that housing prices could not fall dramatically."

high-risk mortgage loans and lending practices/lending

In the years before the crisis, the behavior of lenders changed dramatically. Lenders offer more loans to high-risk borrowers, including illegal immigrants. Loan standards deteriorated mainly between 2004 and 2007, as the government-sponsored mortgage market share of the GSE (ie parts of Fannie Mae and Freddie Mac, specialized in conventional, non-subprime mortgage) decreased and private securitization stocks grew, to more than half of the mortgage securitization.

Subprime mortgages grew from 5% of total origination ($ 35 billion) in 1994, to 20% ($ 600 billion) in 2006. Another indicator of the "classic" boom-bust credit cycle, is the closing difference between subprime and prime mortgage interest rate ("subprime markup") between 2001 and 2007.

In addition to considering high-risk borrowers, lenders have offered riskier loan options and borrowed incentives. In 2005, the average down payment for first-time home buyers was 2%, with 43% of the buyers not paying a down payment at all. By comparison, China has a payment requirement of more than 20%, with a higher amount for non-primary residence.

To generate more mortgages and more securities, credit qualification guides are becoming looser. First, "declare income, verified assets" (SIVA) loan supersedes proof of income with that "statement". Then, "no income, verified assets" (NIVA) loans eliminate proof of employment requirements. Borrowers only need to show proof of money in their bank account. "No Revenue, No Assets" (NINA) or Ninja Loans eliminates the need to prove, or even to declare assets owned. All that is required for a mortgage is the credit score.

This type of mortgage becomes more risky as well. Interest rates are only mortgage rates (ARM), allowing homeowners to pay only the (non-principal) interest of the mortgage during the initial "teaser" period. Even more lenient is the "payment option" loan, in which the homeowner has the option to make a monthly payment that does not even cover the interest for the first two or three years of the initial period of the loan. Nearly one in 10 mortgage borrowers in 2005 and 2006 took this "ARM option" loan, and it is estimated that one-third ARM originating between 2004 and 2006 has a "temptation" rate below 4%. After the initial period, the monthly payment may double or even triple.

The proportion of subprime ARM loans made to people with credit scores high enough to qualify for a conventional mortgage with better requirements increased from 41% in 2000 to 61% in 2006. In addition, mortgage brokers in some cases received incentives from the giver loans to offer subprime ARM even for those who have credit ratings that deserve a loan (ie, non-subprime).

Standard underwriting mortgages dropped dramatically during the boom period. The use of automatic loan approval allows loans to be made without proper reviews and documentation. In 2007, 40% of all subprime loans were generated under automated underwriting. Chairman of the Association of Mortgage Bankers claims that mortgage brokers, while profits from the booming home loan, are not enough to check whether the borrower can repay. Mortgage scams by lenders and borrowers are increasing enormously.

The Financial Crisis Investigation Commission reported in January 2011 that many mortgage lenders take a loyal borrower's qualification on conviction, often by "deliberately ignoring" the borrower's ability to pay. Nearly 25% of all mortgages made in the first half of 2005 were "interest-only" loans. During the same year, 68% of "ARM option" loans originating from Countrywide Financial and Washington Mutual had low requirements or no documentation.

At least one study has shown that the decline in standards is driven by a shift in mortgage securitization from a tightly controlled duopolist to a competitive market in which the most unstable mortgage initiator holds. The worst vintage mortgage years coincided with the period in which the Government Sponsored Business (specifically Fannie Mae and Freddie Mac) were at their weakest, and mortgage lenders and private label securitizers were at their strongest.

Why is there a market for these low-quality private label securities? In the Peabody Award winning program, NPR correspondents argue that "Giant Pool of Money" (represented by $ 70 trillion in fixed income investment worldwide) is looking for higher yields than offered by US Treasury bonds early in the decade. Furthermore, this collection of money has doubled in size from 2000 to 2007, but relatively safe supplies, income-generating investments do not grow rapidly. Wall Street investment banks responded to this demand with financial innovations such as mortgage-backed security (MBS) and collateralized debt obligation (CDO), which are ranked safely by credit rating agencies.

As a result, Wall Street connects this collection of money to the mortgage market in the US, at enormous costs imposed on them throughout the mortgage supply chain, from mortgage brokers selling loans, to small banks that fund brokers, to huge investments banks behind them. Around 2003, mortgage inventories sourced from traditional lending standards have been exhausted. However, continued strong demand for MBS and CDO began lowering loan standards, as long as mortgages could still be sold along the supply chain. Finally, this speculative bubble proved unsustainable. NPR describes it like this:

The problem is that even though house prices go through the roof, people do not make more money. From 2000 to 2007, the average household income remained flat. So the more prices go up, the more loose it all. No matter how skimpy the loan standards are, no matter how many exotic mortgage products are made to sho survivors home that they can not buy, no matter what the mortgage machine is trying, people can not swing it. By the end of 2006, the average home cost was almost four times that of the average family. Historically it was between two and three times. And mortgage lenders are aware of something they hardly ever saw before. People would close a house, sign all the mortgage letters, and then default on their first payment. No job loss, no medical emergency, they are under water before they start. And although no one can really hear it, it may be a time when one of the biggest speculative bubbles in American history emerges.

Subprime mortgage market

Subprime borrowers typically have a weak credit history and reduced repayment capacity. Subprime loans have a higher default risk than loans to major borrowers. If the borrower owes in making timely mortgage payments to the lender (bank or other financial firm), the creditor may take ownership, in a process called foreclosure.

The value of American mortgage subprime was estimated at $ 1.3 trillion in March 2007, with more than 7.5 million sub-prime unpaid first-lien loans. Between 2004 and 2006 the share of subprime mortgages relative to total origination ranged from 18% -21%, compared to less than 10% in 2001-2003 and during 2007. Most subprime loans were issued in California. The explosion in mortgage lending, including subprime loans, was also spurred by the rapid expansion of non-bank independent mortgage proponents who despite their smaller share (about 25 percent in 2002) in the market have contributed about 50 percent of the rise in mortgage loans between 2003 and 2005. In the third quarter of 2007, ARM subprime only reached 6.9% of outstanding US mortgages also accounted for 43% of the foreclosures that began during the quarter.

In October 2007, about 16% of subprime adjustable-rate mortgages (ARMs) were 90-day arrears or lenders had started the foreclosure process, roughly triple the 2005 level. In January 2008, the delinquency rate had risen to 21% and in May 2008 the number was 25%.

According to RealtyTrac, the value of all unpaid housing mortgages, which are owed by US households to buy residential homes for at most four families, was US $ 9.9 trillion by the end of 2006, and US $ 10.6 trillion by mid-year 2008. During 2007, lenders have begun the foreclosure process on nearly 1.3 million properties, an increase of 79% over 2006. This increased to 2.3 million in 2008, an increase of 81% vs 2007, and again to 2.8 million in 2009, an increase of 21% vs 2008.

In August 2008, 9.2% of all outstanding US mortgages, either delinquent or foreclosure. As of September 2009, this has increased to 14.4%. Between August 2007 and October 2008, 936,439 US residents completed the foreclosure. Foreclosures are concentrated in certain countries both in terms of number and foreclosure seizure rates. Ten countries accounted for 74% of foreclosure filings during 2008; the top two (California and Florida) represent 41%. Nine countries are above the national average foreclosure rate of 1.84% of households.

Mortgage scam and predatory borrowing

"The FBI defines mortgage fraud as 'a deliberate misrepresentation, misinterpretation, or negligence by the applicant or other interested parties, relied upon by the lender or underwriter to provide funds for, buy, or to insure a mortgage loan.'" In 2004, The Federal Bureau of Investigation warned of an "epidemic" in mortgage scams, an important credit risk of nonprime mortgage lending, which, they said, could lead to "problems that could have many impacts like the S & L crisis." Nevertheless, the Bush administration prevented the state from investigating and prosecuting predatory borrowers by applying the banking law from 1863 "to issue a formal opinion preempting all the country's predatory lending laws, thus making them invalid."

The Financial Crisis Investigation Commission reported in January 2011 that: "... mortgage scams... flourish in a loosely lending standards environment and loose regulation Number of reports of suspicious activity - reports of possible financial crimes filed by depositors and their Affiliates - linked to mortgage frauds grew 20-fold between 1996 and 2005 and then increased more than doubled between 2005 and 2009. One study puts a loss due to fraud on mortgage loans made between 2005 and 2007 of $ 112 billion.

"Fraudulent lending represents unfair, deceptive, or fraudulent practices of some lenders during the loan origination process." Lenders make loans that they know are incapable borrowers and that can cause huge losses for investors in mortgage securities. "

Financial markets

Boom and collapse of the shadow banking system

Financial Crisis Investigation Commission reported in January 2011:

"At the beginning of the 20th century, we set up a series of protections - the Federal Reserve as a lender of last resort, federal savings insurance, sufficient regulation - to provide defense against the panic that regularly engulfed the American banking system in the 19th Century. Over the past 30 years, we have allowed the growth of shadowy banking systems and loaded with short-term debt - which rival the size of the traditional banking system.Marketing components - for example, the multitrillion dollar repo loan market, off-balance-sheet entities, and the use of over- the-counter - is hidden from view, without the protection we have built to prevent financial ruin We have a 21st century financial system with 19th century protection. "

In a June 2008 speech, NY Federal Reserve Bank President Timothy Geithner, who later became Minister of Finance, put a significant error for freezing credit markets on "run" on entities in the "parallel" banking system, also called the shadow banking system. These entities become important for credit markets that support the financial system, but are not subject to the same regulatory control as depository banks. Furthermore, these entities are vulnerable because they borrow short-term in the liquid market to buy long-term, illiquid and risky assets. This means that disruptions in the credit market will make them subject to rapid deleveraging, selling their long-term assets at depressed prices.

Repos and other forms of banking shadow accounted for about 60% of "the entire US banking system," according to Paul Krugman. Geithner describes his "entity":

"In early 2007, asset-backed commercial paper channels, in structured investment vehicles, in auction-auctioned securities, tender option bonds, and variable rate demand records, had a combined asset size of about $ 2.2 trillion, which was funded overnight at the triparty repo grew to $ 2.5 trillion.Hot assets held in hedge funds grew to around $ 1.8 trillion, a combined balance of five major investment banks totaling $ 4 trillion.In comparison, the total assets of the top five bank holding companies in the United States at the time, just over $ 6 trillion, and the total assets of the entire banking system were around $ 10 trillion. "

He stated that "the combined effect of these factors is the financial system vulnerable to asset prices and self-reinforcing credit cycles." Nobel laureate economist Paul Krugman described the run of the shadow banking system as "the essence of what is happening" to cause the crisis.

As the shadow banking system evolves to rival or even surpass the conventional banking in importance, politicians and government officials should realize that they re-create the kind of financial vulnerability that makes the Great Depression possible - and they should respond by extending the rules and financial safety nets to cover institutions - this new institution. Influential figures should announce a simple rule: anything that does what the bank does, anything that should be saved in a crisis like a bank, should be organized like a bank.

He refers to the lack of this control as "malign neglect."

The securitization market supported by the shadow banking system began to close in the spring of 2007 and nearly died in the fall of 2008. More than a third of the private credit market became unavailable as a source of funds. According to the Brookings Institution, the traditional banking system did not have the capital to close this gap in June 2009: "It takes years of strong profit to generate enough capital to support additional loan volume." The authors also point out that some forms of securitization "are likely to disappear forever, have become artifacts from overly loose credit conditions."

Economist Gary Gorton wrote in May 2009:

Unlike the historical banking panic of the late twentieth and early nineteenth century, today's panic of banking is a huge panic, not a retail panic. In previous episodes, depositors ran to their banks and asked for cash instead of their checking accounts. Unable to meet these demands, the banking system went bankrupt. The current panic involves finance companies "walking" on other financial firms by not renewing repo or repo agreements or repo margins, forcing large deleveraging, and leaving the banking system bankrupt.

Fed Chairman Ben Bernanke said in an interview with FCIC during 2009 that 12 of the 13 largest US financial institutions were at risk of failure during 2008. The FCIC report did not identify which of the 13 companies not considered by Bernanke were in danger of failure.

Economist Mark Zandi testified to the Commission of Financial Crisis Investigations in January 2010:

The securitization market also remains disrupted, as investors anticipate more loan losses. Investors are also unsure about changes in the coming laws and accounting rules and regulatory reforms. The issuance of private bonds from residential and commercial mortgage-backed securities, asset-backed securities, and CDO peaked in 2006 by nearly $ 2 trillion... In 2009, private issuance was less than $ 150 billion, and almost all of it was a supported asset supported by the TALF Federal Reserve program to help credit card, car and small business lenders. The issuance of securities and housing-backed mortgages and commercial housing remains inactive.

The Economist reported in March 2010: "Bear Stearns and Lehman Brothers are crippled non-bankers amongst the panicked overnight" repo "borrowers, many of whom are money market funds unsure about the quality of securities collateral which they hold.The mass redemption of these funds after Lehman's failure to freeze short-term financing for large corporations. "

Securitization

Securitization - the bundling of bank loans to create tradable bonds - began in the mortgage industry in the 1970s, when Government Sponsored Enterprises (GSEs) began collecting relatively secure, conventional, "adjust" or "prime" mortgages, creating "mortgage- backed "securities" (MBS) from the pool, selling them to investors, securing these securities/bonds against defaults on the underlying mortgage.The originate-to-distribute model has advantages over the old "originate-to-hold" model where the bank comes from loans to the borrower/homeowner and maintains credit risk (default) Securitization removes loans from bank books, allows banks to keep complying with capital requirements laws More loans can be made with the proceeds of sales of SBM The liquidity of the national mortgage market and even internationally allows capital to flow where mortgages are in demand and funding is short, but securitization I created a moral danger - banks/institutions that make loans no longer have to worry if the mortgage is paid off - giving them an incentive to process mortgage deals but not to ensure their credit quality. The bankers no longer work to overcome the borrower's problems and minimize the failure during the credit term.

With the high down payment and the credit score of the appropriate mortgage used by the GSE, this danger is very minimal. But the investment bank, wants to enter the market and avoid competition with the GSE. They do so by developing mortgage-backed securities in the subprime market and the more risky Alt-A. Unlike the GSE, issuers generally do not guarantee securities against defaults of the underlying mortgages.

What this "private label" or "non-agency" does is use "structured finance" to create securities. Structuring involves "deductions" of mortgages combined into "tranches", each having different priorities in the principal and quarterly flow of interest and interest. Tranches are compared to "buckets" that capture the "water" of principal and interest. More and more senior buckets do not share the water with the ones below until they are filled to full and overflowing. This provides a great opportunity for credit/tranche tops (in theory) that will get the highest "triple A" credit rating, enabling them to be sold to money markets and pension funds that will not deal with subprime mortgage securities.

To use the lower MBS sections in a three-A-rated non-assessable priority and that the conservative fixed income market will not buy, the investment bank develops another security - known as a secured debt bond (CDO). Although the CDO market is smaller, it is very important because unless a buyer is found for non-triple-A or "mezzanine" tranches, it will not be profitable to create a mortgage backed security in the first place. This CDO collects the remaining BBB, A-, and others. Rate tranches, and generate new tranche - 70% to 80% of them are rated triple A by rating agencies. The remaining 20-30% mezzanine tranches are sometimes purchased by other CDOs, to create so-called "CDO-Squared" securities that also produce tranche with most triple A ratings.

This process was then underestimated as "value laundering" or how to turn "garbage into gold" by some business journalists, but was justified at the time by the belief that house prices would always go up. The models used by underwriters, rating agencies and investors to estimate the probability of credit defaults are based on the history of credit default swaps, which unfortunately return "less than a decade, the period when house prices soared".

In addition the model - which postulates that the correlation of default risk between loans in securitization pools can be measured in modest, stable, constituent amounts, suitable for risk management or assessment - is also intended to show that mortgages in CDO pools are well diversified. or "uncorrelated". The default on a mortgage in Orlando, for example, is considered to have no effect on - ie not correlated with - the real estate market across the country in Laguna Beach. When the price is corrected (ie the bubble collapses), the resulting default is not only larger than predicted but much more correlated.

There are still other innovative security that was criticized after the bubble burst was a synthetic CDO. Cheaper and easier to fabricate than the original "money" CDO, synthetics does not provide funds for housing, but synthetic CDO-purchase buyers who basically provide insurance (in the form of "credit default swaps") against default mortgages. The mortgages they insure are CDO "cash" referenced "synthetics". So instead of providing the investor with interest and principal payments from the MBS tranche, the payment is equivalent to the insurance premium of the "buyer" of the insurance. If the referenced CDO fails, the investor loses their investment, which is paid to the insurance buyer.

Unlike actual insurance, credit default swaps are not regulated to ensure that providers have the backup to pay for the settlement, or that the buyer owns the property (MBS) they insure, ie not just making the security bet will fail. Because synthetics "references" another CDO (cash), more than one - in fact many - synthetics can be made for the same original reference, multiplying the effect if the referenced security fails. Like MBS and other CDOs, the triple A rating for "large pieces" of synthetics is critical to securities success, due to buyer/investor ignorance of the mortgage security market and trust in credit rating agencies ratings.

Securitization began to take off in the mid-1990s. The total number of mortgage-backed securities issued nearly tripled between 1996 and 2007, to $ 7.3 trillion. The subprime mortgage securities (ie, passed on to third party investors through SBM) increased from 54% in 2001 to 75% in 2006. In the mid-2000s when the housing market peaked, the GSE securities market share declined dramatically. , while high-risk subprime and Alt-A mortgage private label securitization grew sharply. When the mortgage default begins to increase, it is among mortgages that are securitized by private banks. GSE mortgage - securitization or not - continues to perform better than other markets. Taking leeway for the reduced CDO cash market was the dominant form of the CDO in 2006, valued "notionally" at around $ 5 trillion.

In the fall of 2008, when the securitization market was "confiscated" and investors would "no longer lend at any price", securities loans comprise about $ 10 trillion from about $ 25 trillion in the American credit market (ie "American homeowners, consumers, and companies owe "). In February 2009, Ben Bernanke stated that the securitization market remained closed effectively, with the exception of fulfilling mortgages, which could be sold to Fannie Mae and Freddie Mac.

According to economist A. Michael Spence: "when previously unrelated risks shifted and became highly correlated... the diversification model failed." "A key challenge ahead is to better understand this dynamic as the analytical foundation of an early warning system with respect to financial instability."

Criticizing the argument that the securitization of intricately structured investments plays an important role in the mortgage crisis, Paul Krugman points out that Wall Street firms issued securities "saving the most risky assets on their own books", and that none of the bubbles are equally catastrophic in European housing or US commercial properties using complex structured securities. Krugman agrees that "debatable is that financial innovation... spreading to financial institutions worldwide" and fragmenting existing loans have made post-bubble "cleanup" through debt renegotiation extremely difficult.

The level of debt and incentives of financial institutions

The Financial Crisis Investigation Commission reported in January 2011 that: "From 1978 to 2007, the amount of debt held by the financial sector jumped from $ 3 trillion to $ 36 trillion, more than doubling as part of gross domestic product. many Wall Street Companies changed - from a relatively quiet private partnership to a publicly traded company with larger and more diverse types of risk In 2005, the top 10 US commercial banks held 55% of industrial assets, more than double the rate which was held in 1990. On the eve of the crisis in 2006, the financial sector's earnings accounted for 27% of all corporate profits in the United States, up from 15% in 1980. "

Many financial institutions, especially investment banks, issued large amounts of debt during 2004-07, and invested proceeds in mortgage-backed securities (MBS), basically betting that house prices will continue to rise, and that households will continue to make mortgage payments. Borrowing at a lower interest rate and investing the proceeds at a higher interest rate is a form of financial leverage. This is analogous to an individual who took a second mortgage at his residence to invest in the stock market. This strategy proved profitable during the housing boom, but resulted in huge losses when house prices began to decline and mortgages began to default. Beginning in 2007, financial institutions and individual investors holding MBS also suffered significant losses from default mortgage payments and impairment of MBS.

The 2004 US Securities and Exchange Commission (SEC) decision related to net capital rules allowed US investment banks to issue much more debt, which was then used to buy SBM. During 2004-07, the top five US investment banks each significantly increased their financial leverage (see diagram), which increased their vulnerability to MBS impairment. The five agencies reported more than $ 4.1 trillion in debt for fiscal 2007, about 30% of the nominal GDP of the US for 2007. Subsequently, the percentage of subprime mortgages derived from total origination increased from below 10% in 2001-03 to between 18-20% from 2004 to 2006, in part due to financing from investment banks.

During 2008, the three largest US investment banks went bankrupt (Lehman Brothers) or sold at fire selling prices to other banks (Bear Stearns and Merrill Lynch). This failure adds to instability in the global financial system. The remaining two investment banks, Morgan Stanley and Goldman Sachs, opted to become commercial banks, thus subject to more stringent regulations.

In the years leading up to the crisis, the top four US depository banks moved about $ 5.2 trillion of assets and off-balance sheet obligations into special purpose vehicles or other entities in the shadow banking system. This allows them to essentially bypass existing rules regarding minimum capital ratios, thereby increasing leverage and profit during the boom but increasing losses during the crisis. The new accounting guidelines will require them to return some of these assets to their books during 2009, which will significantly reduce their capital ratios. One news agency estimates this amount between $ 500 billion and $ 1 trillion. This effect is considered a part of the stress tests conducted by the government during 2009.

Martin Wolf wrote in June 2009: "... a big part of what the bank did at the beginning of this decade - off-balance-sheet vehicles, derivatives and 'banking shadow systems' itself - was to find a way round regulation."

The New York State Supervisory Office has said that in 2006, Wall Street executives brought home a bonus of $ 23.9 billion. "Wall Street traders think of bonuses at the end of the year, not their company's long-term health.The whole system - from mortgage brokers to Wall Street risk managers - seems to be leaning toward taking short-term risks while ignoring the long-term obligations. is that most of the people above the bank do not really understand how that [investment] works. "

Incentive compensation from merchants is focused on the costs resulting from assembling financial products, rather than product performance and profits generated over time. Their bonuses are heavily tilted toward cash rather than stocks and are not subject to "claws" (recovery bonuses from employees by the company) in the case of MBS or CDOs that are not working. In addition, the increased risk (in the form of financial leverage) taken by large investment banks is not adequately considered in senior executive compensation.

Credit default Swap

Credit default swaps (CDS) are financial instruments that are used for hedging and protection for debtor, especially SBM investors, from default risk, or by speculators to benefit from default. Since the net worth of banks and other financial institutions is deteriorating due to losses associated with subprime mortgages, it is likely that those who provide protection should pay their partner partners. This creates uncertainty throughout the system, as investors wonder which companies will be required to pay to cover the mortgage default.

Like all swaps and other financial derivatives, CDS can be used to protect risks (in particular, to ensure creditors against defaults) or to benefit from speculation. The volume of CDS in circulation increased 100-fold from 1998 to 2008, with an estimated debt covered by CDS contracts, as of November 2008, ranging from US $ 33 to $ 47 trillion. CDS is set lightly, largely due to the Commodity Futures Modernization Act of 2000. Since 2008, there is no central clearing center to honor CDS if the parties of the CDS are found to be unable to perform their obligations under the CDS contract. Required disclosure of CDS related obligations te

Source of the article : Wikipedia